Forever and ever

Perpetual futures have landed in America… and have the potential to re-orient finance as we know it

Perpetual futures are having a moment.

You can now buy a leveraged, never-expiring bet on the price of SpaceX, trade it around the clock, and do all of this before SpaceX went public and has no ordinary market price at all. The contract settles in cash. This spring it implied a $1.78 trillion valuation for the company and did about $33 million of volume on its first day.

The instrument that makes this possible is the perpetual future, and it has been turning up everywhere this year. In March, S&P Dow Jones Indices granted Trade[XYZ], a Hyperliquid-based platform, the first officially licensed S&P 500 perpetual contract, available 24/7 onchain to non-US investors. Two months later, the same platform launched two wave-making pre-IPO perpetuals: Cerebras and SpaceX.

These instruments successfully discovered Cerebras’ price days before the IPO, and the SpaceX perpetual is now set at a $1.78 trillion implied valuation, doing roughly $33 million of volume on day one. Coinbase, Binance, OKX, Bitget, Crypto.com and others followed within weeks with their own pre-IPO products. Hyperliquid, the venue underneath much of this, briefly hit a record 6.63% share of global perpetual volume against centralized exchanges in May, with its share against Binance specifically reaching 14.4%.

Then, the perp phenomenon came onshore. On May 29, the CFTC approved Kalshi’s bitcoin perpetual, the first regulated perpetual futures contract available to US persons. Six days later, CME Group’s chief executive Terry Duffy stood up at the Piper Sandler conference and called the approval “a disaster waiting to happen.”

These products have, for most of their existence, traded offshore. That is changing fast. Crypto-native firms are finding new things to write a perpetual on, the old guard is alarmed in public, and an entire product class is going mainstream. Two things this piece will argue:

If and when equity perpetuals arrive onshore, they will be felt at once, because the speculative wallet they slot into is already enormous.

The engineering itself, what a perpetual fundamentally requires, points at a future where anything measurable, with a continuous reference, can have a contract written on it.

Perps are a phenomenal product

Robert Shiller proposed the perpetual future in 1993, in a Journal of Finance paper about how to cash-settle derivatives on illiquid things like real estate that have no clean way to deliver. The idea mostly sat there for more than twenty years. Then in 2016 a crypto exchange called BitMEX shipped a perpetual swap on bitcoin and built one of the defining financial products of the following decade.

A perpetual is a futures contract with the expiration date taken out. That sounds like a small change, but it isn’t.

A normal future settles on a fixed date: you agree today to exchange something at a set price three months out, and on that date the contract resolves and disappears. To hold the position past then you sell the expiring contract and buy the next one, which costs money and attention every quarter. A perpetual never expires, so there’s nothing to roll. The position just sits there for as long as you want it.

The catch with a contract that never settles is that nothing obvious holds its price to the thing it tracks. A normal future converges to spot because it settles against spot; remove that and the two could drift apart. Perpetuals handle it with a funding rate, a small payment that passes between longs and shorts every eight hours or so. When the perpetual trades above spot, longs pay shorts, which makes holding a long more expensive and nudges the price down; when it trades below, shorts pay longs. The funding rate is the tether, doing the job an expiration date does in a normal future, except it never stops.

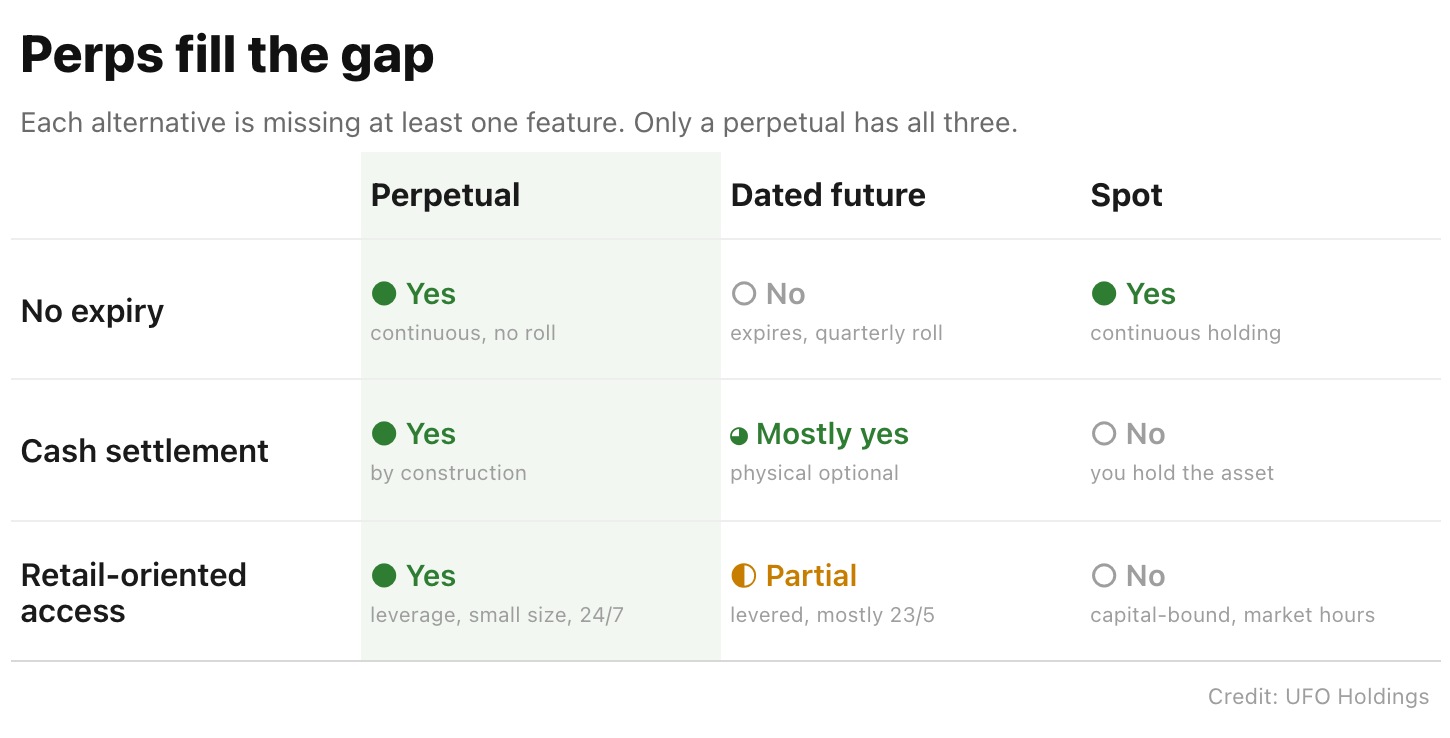

Three features define a perpetual, and no single one of them is unique. It never expires, so there’s no roll and no calendar fragmentation, just one book of liquidity on one instrument. It settles in cash, so there’s no delivery and nothing to custody. And it was built for retail: leverage in both directions, small position sizes, round-the-clock trading, no friction to short. Dated futures are cash-settled and levered. Spot trades continuously and never expires. What no other product manages is all three at once.

Which feature does the real work depends on what you put the perpetual next to. Against a dated future, the one that matters is no expiry. The dated contract already settles in cash and already offers leverage, so the perpetual adds little there; what it adds is the end of the roll and the concentration of liquidity into one book rather than four quarterly contracts on a curve. Against spot, the comparison flips. Spot is already continuous, so no expiry is the shared feature this time, and the perpetual’s edge is cash settlement and the retail bundle: leverage, easy shorting, no custody.

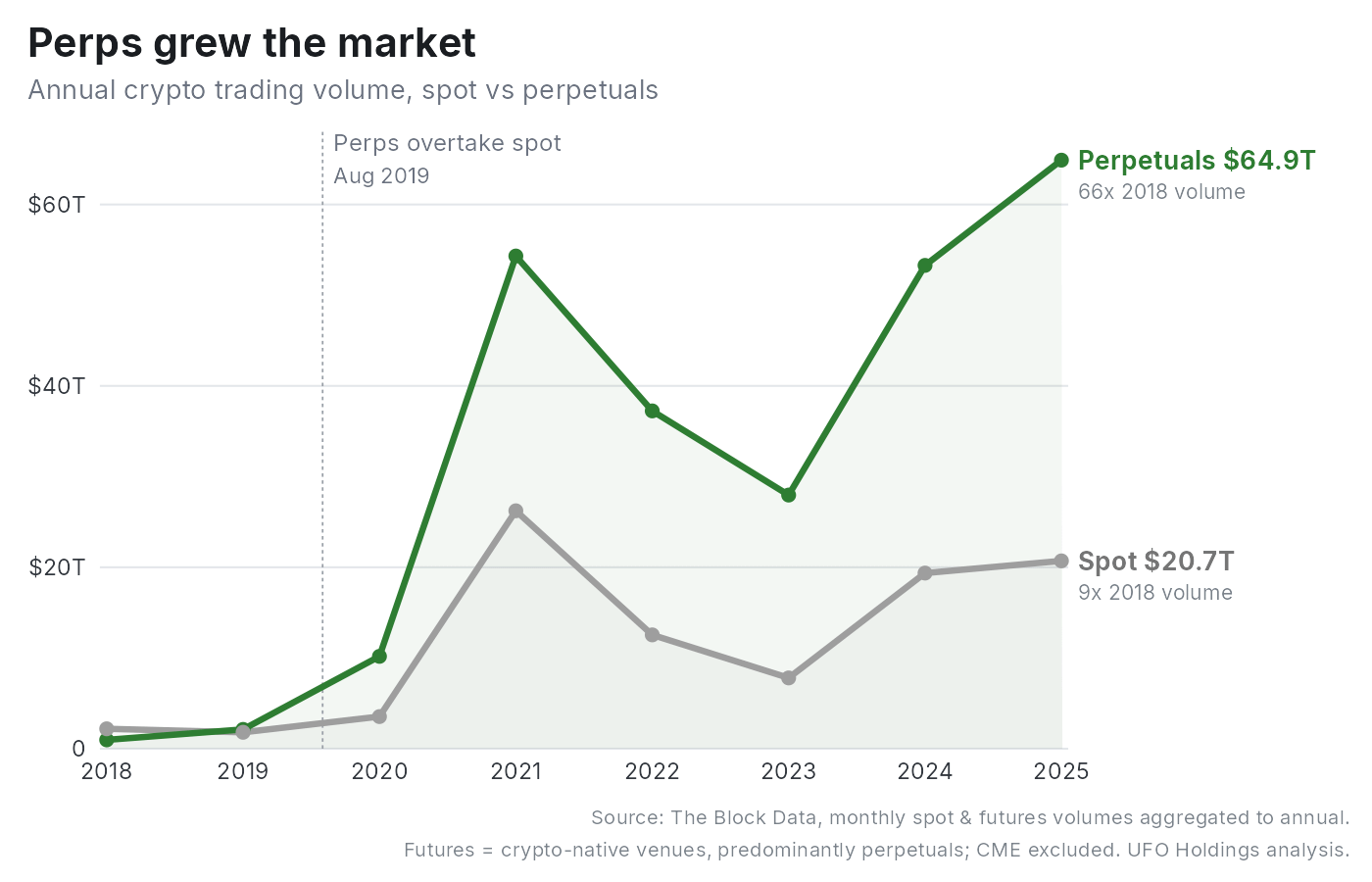

Crypto was the case where all three features won against both alternatives at once, which is why perpetuals took over crypto. Dated crypto futures had thin liquidity; crypto spot was clumsy to short and a chore to custody. The perpetual beat both comparisons cleanly. Today perpetuals are around three-quarters of all crypto trading, and global perp volume ran past $60 trillion in 2025, several times the spot market they derive from. People would rather trade the derivative than the thing itself.

There’s a cost buried in the design, and it’s the part most people skip. Continuous leverage needs a way to absorb a position that blows through its margin before the exchange can close it, which is what happens in a fast market.

Offshore venues use auto-deleveraging: when a blown-up trader can’t cover the loss, the exchange force-closes winning positions on the other side to square the book1. Retail tolerates that, since the worst case is a winning trade cut short and nobody loses more than they put in.

US central clearing runs losses the other way, through a capital waterfall: the failed broker first, then the clearing house’s guaranty fund, then the surviving members backstopping one another. That last step is the one institutions can’t accept, because no clearing member wants to be on the hook for a competitor’s customers. The same contract is a different animal depending on which machine sits behind it.

This is a subtle, but perhaps the most interesting wrinkle around on-shored perpetuals in a DCM. ADL is something that crypto traders have grown to accept as it was necessary for a decentralized exchange.

All of this stayed offshore for most of a decade. The interesting question is what happens when it shows up somewhere it hasn’t been allowed before.

Public markets clue us into the disruption at stake

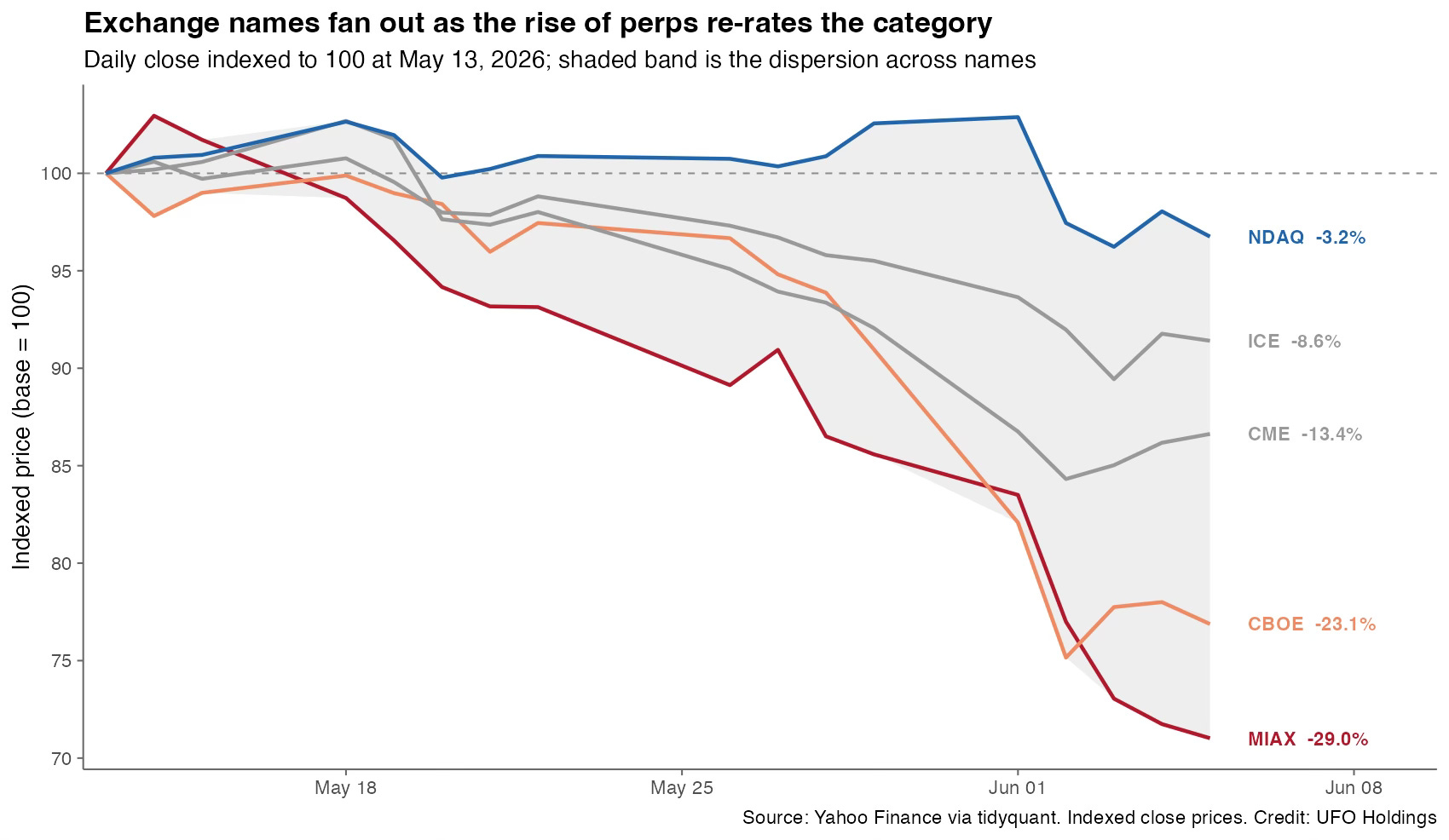

When the CFTC approved that first bitcoin perpetual on May 29, the price reaction worth watching showed up somewhere odd: in the share prices of the companies that run America’s options and futures exchanges.

What the market was pricing is the chance that perpetuals come for their business, and it was sorting the exchanges by how exposed each one looked. The interesting part is what “exposed” turns out to mean.

You’d guess the exchanges most at risk are the ones running cash-settled products, since a perpetual settles in cash. That’s half right, and the half it misses is the half that matters. Picture what a perpetual is from a trader’s seat: a leveraged, short-term, directional bet that pays out in cash and never makes you take delivery of anything.

Two things are true about that bet at once. It is the kind of thing a retail trader reaches for, and it settles in cash. A product only competes with it if it does both. Cash settlement without a retail audience is just plumbing for institutions. A retail audience whose product hands you the underlying, single-stock options that settle in shares, sits one step removed from what a perpetual replaces. The flow a perpetual actually eats is retail-facing and cash-settled at the same time.

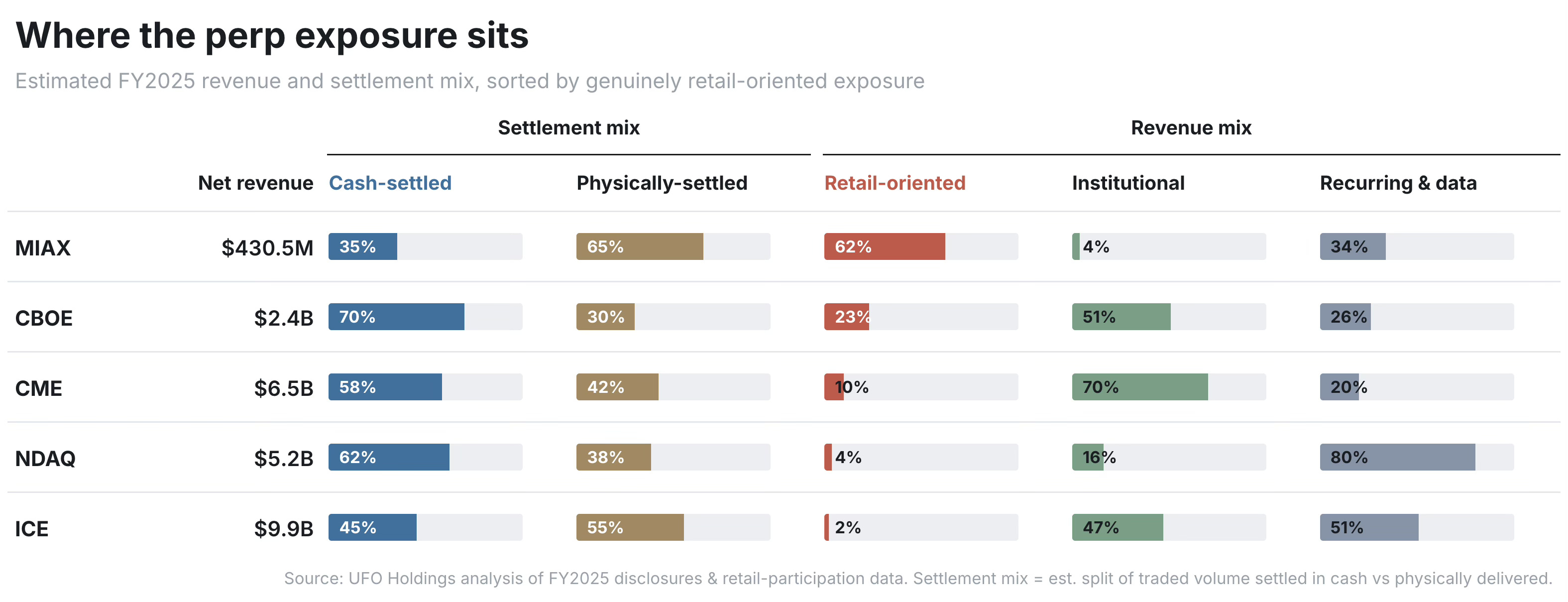

MIAX took the worst of it because it is the closest thing on the list to a pure retail-options business, with almost nothing else on the income statement to absorb a hit. Sixty-two cents of every revenue dollar rides on short-dated, retail-oriented order flow.

CBOE’s retail share it look modest, under a quarter of revenue, and a retail-only read would have it falling far less than MIAX. It fell nearly as hard. The reason is that CBOE’s retail flow is the most perfectly perp-shaped flow on the board.

Its franchise is SPX and VIX, cash-settled index options, much of it zero-days-to-expiry: short-dated, leveraged directional bets that settle in cash, which is a perpetual with an expiration date stapled on.

Seventy percent of CBOE’s traded volume settles in cash, the highest share on the list, and the retail slice of it is exactly the slice a perpetual takes first. The same logic sorts the ones that held up.

So the public market has already decided perpetuals matter. It hasn’t yet had to ask whether they’re legal.

The regulatory door is ajar

Here’s something most people who follow markets don’t know: you can’t trade a futures contract on Tesla. Not on Apple, not on Nvidia, not on any single US stock. You can trade options on Tesla, you can trade an S&P 500 future that holds Tesla, you can buy the shares outright. The one thing you can’t do is trade a future on Tesla by itself. The reason is statutory, and it goes back decades.

From 1981 to 2000, futures on single stocks and on small baskets of stocks were flatly illegal in the United States. In 2000 Congress lifted the ban, but only halfway: these products became legal on the condition that the SEC and the CFTC regulate them jointly, with both agencies’ rulebooks applying at the same time. A dedicated exchange spent 18 years trying to make the joint-regulation version work and shut down in 2020 having gone basically nowhere. Broad-based index futures, the S&P 500 kind, got carved out and left to the CFTC alone, which is why those trade freely while single-stock futures effectively don’t exist. That was the state of things until a few weeks ago.

Three things have happened since late May, and together they point in one direction.

The first is the policy statement the CFTC put out on May 29, alongside its approval of the bitcoin perpetual. Most of it concerns how the agency will review perpetual contracts: case by case, rather than through the self-certification process exchanges normally use to list something new. The part that matters is the agency’s reading of a rule called Core Principle 3, which says a listed contract can’t be readily susceptible to manipulation. Here is how the Commission applied it to perpetuals:

For a traditional, cash-settled futures contract, the susceptibility-to-manipulation analysis directed at the cash settlement reference price is an analysis of one moment in time: the settlement reference price must be reliable at expiry. For a perpetual contract, however, the reference must be reliable at every funding interval, without interruption, for as long as the contract remains active.

That’s a higher bar than any dated future has to clear, and it’s written with nothing crypto-specific about it. The same is true of the asset classes the document says the framework could cover: “agricultural products, precious metals, equity securities, and narrow-based security indexes.” Equity securities and narrow-based indexes are precisely the things the statute prohibits without joint SEC-CFTC sign-off. The CFTC didn’t have to mention them, but it did anyway.

The second thing happened the same day. The CFTC issued a no-action letter letting Coinbase route US clients to perpetuals listed on Deribit, an offshore exchange, by treating those contracts as foreign futures. The mechanics cover crypto only, so this doesn’t reach equities. The point is the method: the agency used its own discretionary authority to pull an offshore product onshore, without waiting for the SEC and without new legislation. It’s a tell about how this CFTC moves when it wants something to happen.

The third thing was the chair saying it out loud. On June 8, ten days after the policy statement, the CFTC chair, Mike Selig, went on the Empire podcast and, asked how the two agencies would handle products that straddle their jurisdictions, reached for a specific example: “a regular security like an Nvidia perpetual that actually goes through a process between the CFTC and the SEC.” He sketched a rough order of operations in the same conversation. Crypto perpetuals get a fast lane through exchange self-certification now that the template exists. Securities, single stocks included, go through a joint process with the SEC. Physical commodities like grain and metals aren’t coming soon. The mechanism he kept returning to was “substituted compliance,” letting one primary regulator clear a product that would otherwise answer to two.

None of this makes equity perpetuals legal today. It does tell you that the people who would have to allow them are working out how. The market is thinking a step ahead, which raises the next question: if this door ajar swings wide open, how big does it get?

How big this gets in equities

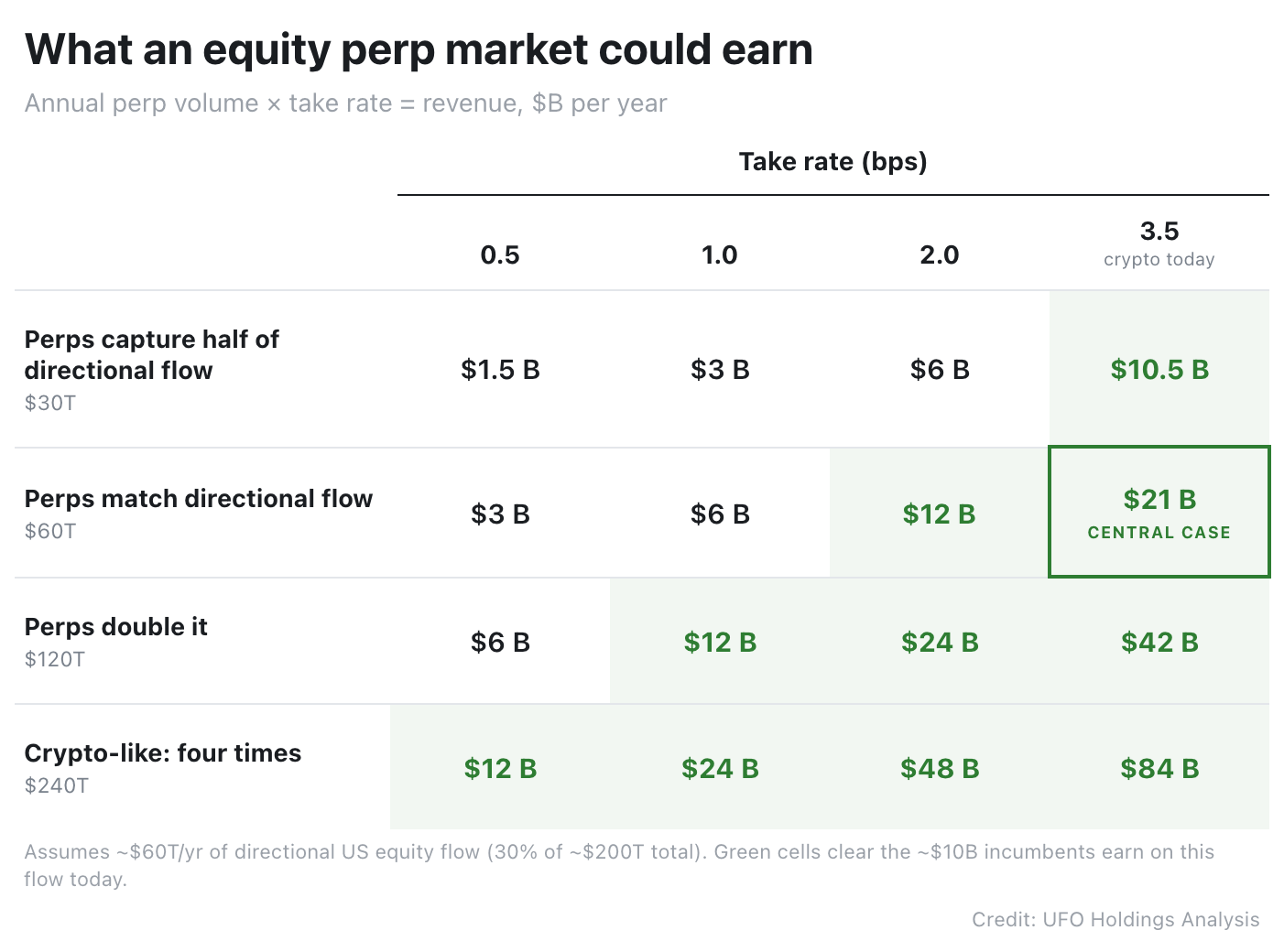

There are two honest ways to size this, and they land on very different numbers, so it’s worth doing both.

The smaller number is what already exists. Add up the fees sitting on US equity directional flow today: the options exchanges, the clearing house, the payment for order flow, the commissions, and CME’s equity-index futures business. It comes to roughly $10 billion of revenue a year, maybe $15 to $20 billion counting the spread market-makers earn on the same flow.¹ Call that the floor: what a perpetual redirects if it does nothing more than take share, and the number I’d defend if I only got to defend one.

The bigger number comes from asking what perpetuals did the last time they turned up somewhere new. In crypto, they grew the market.

The product pulled in activity that hadn’t existed before it. The front edge of the same effect is already visible in equities: 0DTE options, contracts that expire the day they trade, went from almost nothing five years ago to a quarter of all US options volume. Retail turns out to have a large and previously unmet appetite for simple, leveraged, short-term bets.

Equities probably won’t go as far as crypto did, though. Most US equity trading is ownership rather than speculation. Pension funds hold equities to match liabilities, index funds hold them because their investors paid for exactly that exposure, and the tax code pays retail to sit still. None of those people have any use for a cash-settled perpetual, which gives you the price and no claim on the asset. So whatever multiple of spot the equity perp market reaches, it applies only to the slice of trading that’s actually directional. Call that 30% if you want a number, though I’d take a higher or lower one from somebody who’s thought about it harder than I have.

From there the arithmetic is short: directional flow, times whatever volume perps reach against it, times the fee.

The fee a competitive perpetual can charge matters more than how big the market gets, and crypto’s fee has been falling the whole time. The cells that clear the roughly $10 billion incumbents already earn on this flow are the ones worth arguing about, because that’s the line between eating the existing pie and growing it.

If this still reads as speculative, it’s already happening, just not here. Hyperliquid did about $11 billion of onchain equity-perp volume in 2025, with Nvidia, Tesla, and Alphabet the most active names. Trade.xyz’s S&P 500 perpetual is running at something like a $600 billion annual pace. Equity perp volume across venues grew ninefold in the first quarter of 2026, by BitMEX’s count.

And the contract-for-difference industry, which is leveraged cash-settled equity betting under a different name, has been legal across Europe and Asia for years and banned for US retail under Dodd-Frank, with a handful of public operators earning a couple billion a year from products Americans aren’t allowed to touch. The demand has been demonstrated. The piece that’s been missing is a legal venue at home, and that is the piece that just started to move.

Equities are the loud version of this story. The wallet is enormous, the names are famous, and the disruption shows up in stock prices people already follow. But the rule that opened the door says nothing about equities in particular. It sets a test, the one from the policy statement, and anything with a deep, continuously observed price can pass it.

The honest name for where this points is hyperfinancialization: the CFTC is assembling the machinery to put a tradable contract on more or less any measurable thing, with perpetuals as one vehicle and event contracts as another.

These are just futures with a forced hourly expiration. It’s funny they supposedly have no expiration, when it actuality they expire every hour. When people realize they are paying this funding rate to essentially roll positions in heavy contango every hour, more and more will go back to regular futures. Hmm wonder if there is a play on the CME / CBOE! Wish there were perps available to play those :)

Love this and very informative. Would love to get your color on why CFD as an instrument was/isn’t more heavily used? I have messed around these for a while and they felt very much like Perps on steroids. But when i have asked even the most connected people around the perp and crypto fringes, they aren’t as educated on them.